Publicis paid $2.2 billion for the substrate. The operator question is which deterministic layer you own.

Publicis bought LiveRamp for $2.2B to feed Marcel. That's the holding-company tier publicly pricing a thesis operators have been building toward for two years.

Publicis announced the LiveRamp acquisition on Monday. $2.2 billion enterprise value, $38.50 per share, a 29.8% premium, expected to close by the end of calendar 2026. Trade press has covered it the way trade press covers these things: identity-layer consolidation, post-cookie positioning, scoreboard updates between holding companies. Those framings aren’t wrong. They’re also not the part of this deal worth thinking about.

The part worth thinking about is the sentence Publicis put into the public-facing strategic rationale. “Models and agents are only as useful as the data they can safely act on.” That isn’t deal-press boilerplate. That’s the entire thesis of the deal, and it’s the same thesis that a particular kind of operator team has been quietly building toward for the last two years.

A holding company just publicly priced that thesis at $2.2 billion. That’s the part worth sitting with.

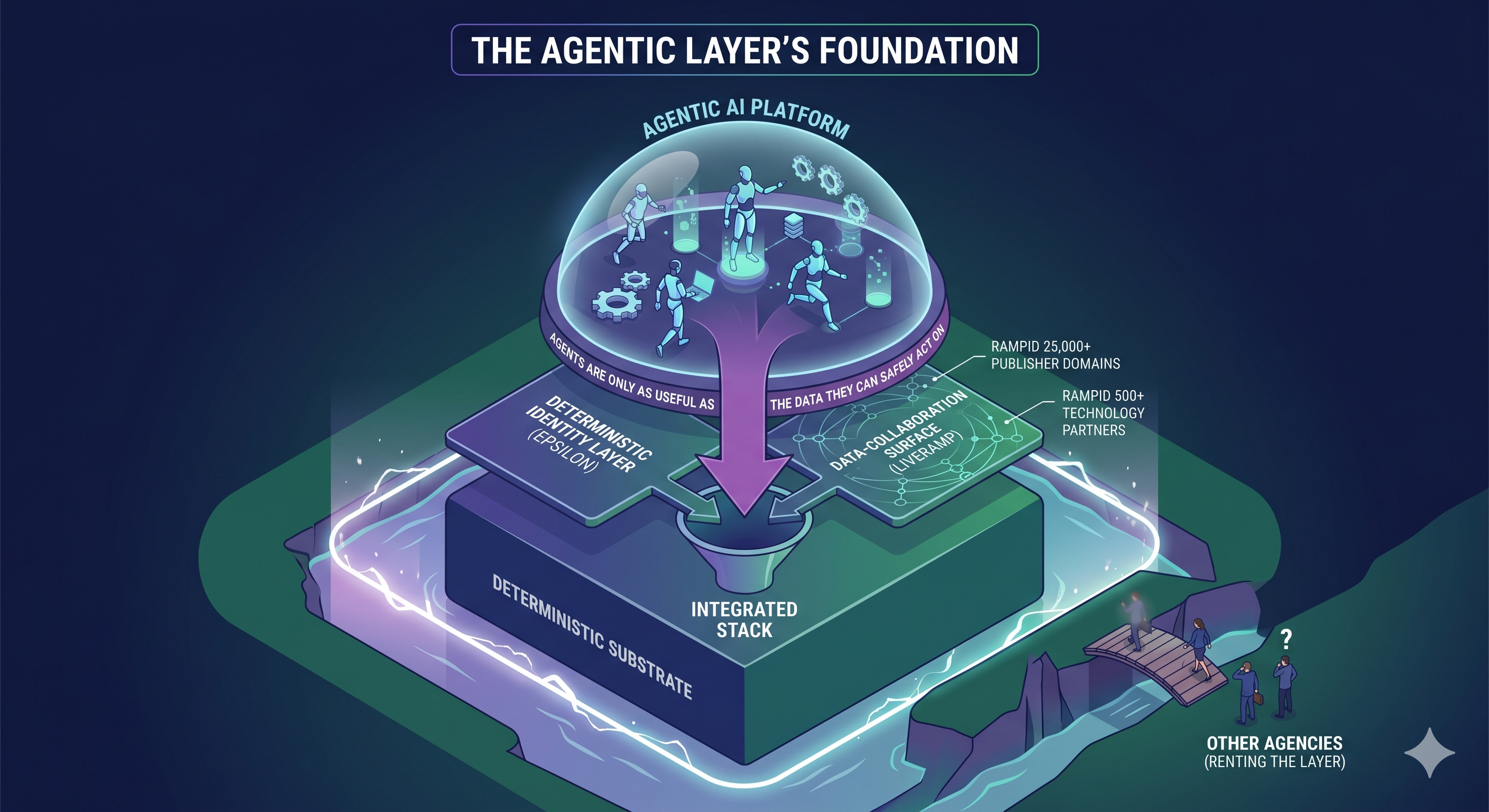

What Publicis actually bought

The integrated stack the deal materials describe is specific. Epsilon, which Publicis already owned, contributes the deterministic identity layer. LiveRamp contributes the data-collaboration surface and RampID, which currently sits at 25,000+ publisher domains and 500+ technology partners. Marcel, Publicis’s agentic platform, is what runs on top of that combined substrate. The agentic layer is the visible product. The deterministic layer underneath is what the $2.2 billion was actually for.

Publicis raised its 2027 and 2028 net-revenue and EPS growth targets on the close. That’s the part of the announcement that tells you what the executive committee actually believes. You don’t raise multi-year guidance on an acquisition unless you think the asset you’re buying is structurally accretive, not just additive. Publicis isn’t buying LiveRamp to bolt it onto the holding-company P&L. They’re buying it because they think the agentic layer they’ve been building on Marcel is worthless without a deterministic substrate they actually own, and they aren’t willing to rent that substrate from a third party going into 2027.

That last point is the operator-tier read.

The question the deal forces

If you run any kind of media or marketing operation, the deal forces a question that’s easy to defer in normal years and impossible to defer in a year where a holding company just paid $2.2 billion to resolve it: which deterministic layer of the marketing path do you actually own?

The honest answer for most agencies is none of them. Most agencies sit on top of platforms other people built. They buy media inside a network’s auction. They measure conversions inside that network’s reporting interface. They build dashboards on top of a third-party analytics tool. They pull lists from a third-party CRM. They report results using a stack of borrowed observability layers, each one owned by an entity whose incentives are not identical to the agency’s. That arrangement is fine when the layer underneath is stable, neutral, and cheap. It stops being fine the moment any of those three properties changes, and all three are changing right now.

The operator-tier alternative isn’t to build everything. Nobody is going to outbuild Publicis on identity, and nobody should try. The alternative is to own the layer of the path that matters most for the specific work you’re paid to do, and to make that ownership structural rather than rented.

There are a few concrete shapes this takes in practice. I’ll describe them generically because the specifics don’t matter for the argument.

One shape is owning the click-to-conversion join. On most networks, the join between an ad click and the resulting conversion is something the agency has to ask the network to surface back. The network has its own attribution model, its own lookback window, its own definition of what counts. When the network reports a number, the agency has to either accept it or argue with it. An agency that owns the join, that controls the tracker, the parameter scheme, and the destination of the click-stream, doesn’t have to argue. They have the underlying data themselves. They can choose which model to apply to it. They can show clients a unified view across networks that no single network’s reporting interface can produce.

Another shape is owning the first-party pipe. Most agencies pass first-party data through a vendor stack and watch it disappear into a black box. An agency that operates its own ingestion, schema, and warehouse for first-party data has a structurally different relationship with that data than one that doesn’t. It can build joins that the vendor doesn’t expose. It can hold data the vendor’s policy doesn’t let it hold. It can apply models the vendor’s roadmap doesn’t include.

A third shape, the one I keep watching get underbuilt across the industry, is owning a proxy in front of partner feeds. Most network partnerships involve a feed flowing from the agency or client into the network’s auction. Standard practice is to send the feed and hope the network’s URL templating respects the parameters you care about. The harder, more valuable shape is to operate a managed service that stands up a proxy in front of the feed, tags every URL in-stream before the feed continues to the network unchanged, and then owns the click-to-conversion join the agency previously had to ask the network for. I know one agency-tier example directly, an agency that has been doing exactly this for clients, and the economics are interesting. Each additional partner is a one-time setup against ongoing margin, and the pattern is reusable across networks. The agency owns the join. The network never knows the difference. The client gets a single deterministic view across partners that no single network can produce.

None of those three shapes are exotic. They’re all variations of the same idea, which is the idea Publicis just paid $2.2 billion for. Own the deterministic layer. Run the agentic layer on top of it. Don’t try to do the second without the first.

The “but Publicis bought it” objection

There’s a counter-argument worth taking seriously, and it’s the strong version, not the weak version. You could read this deal as the exact opposite of what I’m saying. Publicis bought the layer, so the layer is now commodity, so don’t bother building it. RampID will be available. The data-collaboration surface will be sold as a managed service. Why build what you can buy from a holding company that already paid the integration cost on your behalf?

I don’t buy that read, and the reason is in the phrase “models and agents are only as useful as the data they can safely act on.” Publicis didn’t buy LiveRamp because the substrate is a commodity. They bought it because the substrate is the moat. If RampID were going to be cheaply available to every agency that wanted to rent it in 2027, you don’t pay a 29.8% premium and raise multi-year guidance to own it. You pay that premium because you’ve concluded that owning the substrate is the structural prerequisite for your top-line story, and you’d rather not have a competitor able to own it instead.

The same logic runs at the operator tier. The agentic layer is going to commoditize. Anthropic, OpenAI, and Google will keep shipping templates and managed runtimes that get closer every quarter to “press button, get deliverable.” The work on top of those models gets cheaper to do every six months. What doesn’t commoditize is the deterministic data the agentic layer needs to act on. That data has to come from somewhere. Either you own the layer that produces it or you rent that layer from someone who does.

Renting is fine when the rent is low. The question is what happens to the rent when the company you’re renting from concludes, the way Publicis just concluded, that the substrate is the moat.

The specific moment this is happening in

A few weeks ago we sent a formal proposal to a client to stand up exactly the kind of layer I’m describing. Not in those words, and not with the LiveRamp announcement to point to, because the announcement hadn’t happened yet. But the shape of the proposal was: you have a partner feed flowing into a network’s auction. You’re depending on the network to tell you which clicks turned into conversions. We can stand up a layer that owns that join independently. Once we own the join, we can build measurement, optimization, and reporting on a deterministic substrate you control, rather than on a borrowed view from the network.

The proposal sat in the inbox of a client who, like most clients, is being pulled in eight directions at once and would prefer to defer a structural decision in favor of a tactical one. That’s a normal posture in a normal year. It’s a more expensive posture in a year where a holding company just paid $2.2 billion to ratify the structural decision.

The reason the LiveRamp deal matters for operator-tier conversations isn’t that it tells clients to do anything they weren’t already considering. It’s that it gives every operator pitching a deterministic-substrate play a public, $2.2-billion piece of evidence that the thesis isn’t a vendor pitch. It’s a market-clearing price.

What the operator-tier takeaway actually is

The operator-tier read on this week isn’t “we should react to Publicis.” It’s that Publicis just made the slow conversation faster. The conversation about owning a deterministic layer of the marketing path has been happening at most operator teams for two years. It’s a conversation that was easy to defer in a year where the substrate question felt abstract. It’s harder to defer in a year where a holding company just put a $2.2 billion price tag on the answer.

The teams that have been quietly building toward owning a layer have a clearer answer to “what’s our moat in 2027” today than they did last Monday. The teams that haven’t been building toward it now have a public benchmark for what the layer is worth, which is useful information whether you read it as a buy signal or a build signal.

The deeper pattern is the one I keep coming back to in these posts. The infrastructure layer keeps commoditizing. The substrate underneath it keeps being scarce. Every wave of this industry, the value has migrated to whoever owns the layer just below where everyone else is competing. The agentic layer is where everyone is competing now. The deterministic layer underneath it is where the value has migrated. Publicis just paid $2.2 billion to say so out loud.

The interesting question, the one worth carrying out of this week, isn’t whether the thesis is right. The check resolved that for the market. The question is which layer you own, and how quickly you can answer that without flinching.

Only visible to you when signed in. X opens with the post pre-filled. LinkedIn requires a paste — the button copies the text and opens the composer.